Q. Which method shall be applied to calculate the Customs value of the imported goods which are for sale through the e-commerce website?

It should be calculated based on the methods of the Customs valuation of the imported goods, which are from the Primary method to the Fall-back method. Which method should be applied is depending on whether the import transaction exists or not. Therefore, please confirm the role of the importer and facts of the transaction such as person or company to be delivered or to be resold.

Please kindly note that for determining the existence or nonexistence of an import transaction, it should be taken into account not only by the contents of the importer’s explanation (in written form) or attached documents of the import declaration, but also the overall facts of the imported goods, including whether such contents reflect the actual transaction accurately or not.

Q. In case an importer asks a customs broker to take an import clearance procedure on his/her behalf, how should the customs broker make the import declaration when the existence of the import transaction or detail of the transaction of the imported goods is unknown?

An applicable method of the Customs valuation depends on whether it exists an "import transaction" between a seller and a buyer of the imported goods or not. First, please confirm the role of importer such as a buyer, a proxy of buyer located in Japan, a proxy of non-resident, Customs manager under Article 95 of Customs Law as a proxy of non-resident. Also please confirm a place and a person/company to deliver or to resale after importation. Otherwise, it may not be possible to make an import declaration with the correct price.

Furthermore, prior to filing an import declaration, please make sure to obtain the relevant and necessary information to calculate the Customs value and evidence for such calculation.

Q. When the imported goods will be sold through the e-commerce website, is it possible to use an invoice price for an import declaration for Customs valuation purposes?

In case the import transaction exists and the Primary method for the Customs valuation purpose is applicable, it is possible to determine the Customs value based on the invoice price as far as the invoice price correctly represents the price of the import transaction and conditions of such transaction.

For example, when a person/company located in Japan ordered the goods as a buyer, and the goods shipped from the seller who received the order from the buyer and arrived at Japan, it is considered there is an import transaction and Customs value shall be calculated based on the invoice price if the invoice price represents the correct price of the transaction.

Q. In case an importer is a resident of Japan, is it possible to use an invoice price for an import declaration?

Although an importer is a resident of Japan, the Customs value shall be calculated in accordance with Article 4-2 or the Articles following, not applicable to use the invoice price when the goods are imported without import transaction (for example, the buyer is non-resident).

In addition, when the imported goods were exported by a non-resident to sell through the e-commerce website and a proxy of buyer make import declaration as an importer (declarants of import declaration), it is considered that the import transaction does not exist for the imported goods.

More specifically, the nonexistence of the import transaction is applied for cases that an importer takes import relating services or delivery services to the warehouse of the e-commerce website on behalf of an exporter.

Q. How shall the Customs value be calculated if a non-resident imports the goods in order to sell them through the e-commerce website?

In case a seller of the e-commerce website is a non-resident and the goods imports to Japan without a sale between seller in export or producing country and a buyer located in Japan, there is no import transaction and the Primary method is not applicable to calculate the Customs value.

If the Primary method is not applicable, the following alternative methods shall be applied in sequential order:

・the Identical or Similar goods value method (Article 4-2)

・the Deductive value method (Paragraph 1, Article 4-3)

・the Computed value method (Paragraph 2, Article 4-3)

・the Fall-back method (Article 4-4)

Q. In case that the imported goods are sold through the e-commerce website by a non-resident, how shall the Customs value be calculated by using a specific method under the Fall-back method which is set by the Director General of the Customs?

When the specific method set by the Director-General of the Customs under the Fallback method, Article 4-4 shall be applied, such as importer wishes to make the import declaration by the general procedure (not using the BP system) but there is no domestic sale, the Customs value shall be calculated based on the materials submitted to the Customs for import declaration which is considered as objective and reasonable means.

For example, the Customs value can be calculated based on an estimated price of the identical or similar goods on the e-commerce website by recognizing the estimated price as deemed domestic selling price. In this case, the expenses of the domestic costs which are surely confirmed as accurate after arrival in Japan and the Customs duties and taxes at the importation shall be deducted.

Q. In case of applying a method set by the Director-General of the Customs, what kind of materials should be submitted to the Customs?

The materials to be used for the calculation of the Customs value should be based on the objective and reasonable source and truly and accurately indicate the amount that is to be used as the basis of calculation of the Customs value and circumstances of the transaction. Therefore, materials which are simple lists of domestic sales and a series of domestic costs made by an exporter is not sufficient enough as objective and reasonable source of evidence.

If the Customs requests to submit materials of a domestic selling price or domestic transportation costs, please submit materials which verify the domestic selling price on the e-commerce website and an actual invoice to a vender, of which clearly indicates such domestic transportation costs.

Reference: Customs Tariff Law, Japan Customs

Japan Customs: Customs Valuation System

Japan Customs: Details of Japan Customs Valuation System

FTA/EPA, Customs and International Trade Advisory Services

ACP Service for Importer of Record (IOR)

ACP Service for Exporter of Record (EOR)

Customs Support for Transfer Pricing Adjustments

Why choose us?

- Customs and International Trade Professionals - Our CEO, Mr. Sawada, is a Certified Customs Specialist in Japan. With years of experience providing services in the Trade & Customs field, his leadership at KPMG and the establishment of his own company, SK Advisory, ensures our commitment to excellence and high-quality service.

- Full Adherence to Japanese Customs Law - Our top priority is to maintain full compliance with Japanese Customs Law and safely import / export our clients' goods into / from Japan. We meticulously manage all import compliance aspects, including Japan Importer of Record (IOR) matter, HS code classification and the correct Customs Valuation of goods entering Japan. We support to complete all the necessary shipping documents, such as Invoice, Packing List and BL, on behald of non-resident / foreign Japan IOR.

- Communication in English, Chinese, and Japanese - Our team, with extensive international experience, excels in communication in English, including facilitating English-language meetings, and has earned considerable trust from clients. We also have staff capable of communicating in Chinese, making us equipped to handle Chinese-language support as well. Naturally, as a Japan-based team, we're totally fluent in Japanese, ensuring seamless communication across these three key languages.

- Reputable and Reliable Partner -The growing demand for our Attorney for Customs Procedures (ACP) services is testament to our quality. We proudly serve clients globally, registering over 50 ACP customers annually. Our consistent track record underscores our reliability and credibility. For a detailed list of our clientele, please visit our "Experiences" section. Our unwavering commitment ensures all our clients successfully acquire Japan IOR status and import goods seamlessly into Japan.

- Recognized ACP Service Provider on Amazon SPN (Service Provider Network) - We are a certified ACP service provider within Amazon's Service Provider Network (SPN), listed under the Trade Compliance category. Many international Amazon Sellers have successfully become Japan Importers of Record (IOR) through our ACP services.

Our Customers - Japan IOR / Attorney for Customs Procedures (ACP) Service

All our clients have successfully become Japan Importer of Record (IOR) and imported goods into Japan under our guidance.

Logistics Companies with Collaboration Experience

Here is a list of our partner logistics and forwarding companies with whom we have had successful collaborations. Please note that this list is not exhaustive, as we are open to working with any logistics or forwarding companies. As Attorneys for Customs Procedures (ACP), we represent non-resident clients (IOR) and coordinate with these logistics companies, who manage the transportation of goods to and from Japan.

Japanese Customs System Reform: Clarification of Importer Definitions

Starting October 1, 2023, Japanese Customs has instituted a pivotal reform aimed at addressing the issue of foreign sellers improperly designating third parties (such as forwarders or customs agents) as importers.

This revision necessitates foreign corporations to utilize an Attorney for Customs Procedures (ACP) to assume the role of Importer of Record (IOR) directly in many cases. The practice of merely nominally appointing another entity as the importer is no longer feasible.

Notably, foreign corporations that act as importers themselves, through the engagement of ACP, are eligible for Japan Consumption Tax (JCT) benefits. (link: Consumption Tax Treatment and Benefits of Using ACP).

As a dedicated ACP firm, we ensure compliance with the law to facilitate correct import procedures, allowing you to trust us with your importation requirements confidently. We are eager to engage in further discussions with you.

Revisions Effective October 1, 2023:

Definition of the Importer

- Regarding a cargo imported under import transaction, an importer is equivalent to “a person who imports a cargo” defined in Article 6-1 (1), General Notification of the Customs Act. ..... This means, the Consignee, etc., in the case of imports conducted through normal transactions between an overseas seller and a Japanese buyer

- In the cases other than above, an importer is a person who has a right to disposition of the import cargo at the time of import declaration. If there is another person who acts on the purpose of the import*, that person is also included :

In case of a cargo imported:

- under lease contracts, a person who rents and uses the cargo.

- for consignment sales, a person who sells the cargo in the name of himself/herself (consignee) by accepting the commission.

- for processing or repairing, a person who processes or repairs the cargo.

- for disposal, a person who disposes the cargo.

For additional information, please refer to the following resources:

- Japan Customs: Leaflet(English) Revision of Import Declaration Items and Attorney for Customs Procedure (ACP) System

- English: Announcement from Japan Customs | Mandatory to Use ACP in Many Cases – Attorney for Customs Procedure

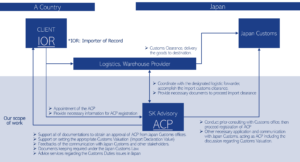

Our ACP Service: The Best Solution for the Japan Importer of Record (IOR)

Attorney for Customs Procedures (ACP) is the best solution for addressing the issue of Japan IOR - Importer of Record. Below is an outline of our primary services and a diagram illustrating the operational structure of the ACP service. Upon successful ACP registration, a foreign entity can become the Japan IOR - Importer of Record.

Basic Scope of Services:

- Consultation with the Japan Customs Office for successful ACP registration.

- Liaising with stakeholders, including Logistics Forwarding Companies and the Customs Offices, on behalf of non-resident clients (i.e., non-resident Japan IOR) to ensure the secure importation of goods.

- Assistance in preparing the necessary documentation for import clearance.

- Support of calculation of Customs Value (Customs Valuation Formula), in accordance with appropriate compliance under the Japan Tariff Customs Law.

- Documents keeping, required under article 95 - Japan Customs Law

**Both import and export activities can benefit from the use of an ACP (Attorney for Customs Procedures). This support is applicable in scenarios where a non-resident acts as the Importer of Record (IOR) for imports and as the Exporter of Record (EOR) for exports.

Three Steps to Initiate Shipments Under the ACP Program: :

- Quotation Review to Contract Conclusion: Upon receiving your contact details, we will promptly provide a quotation for your review.

- Commencing the Registration of ACP (Attorney for Customs Procedure) to Japan Customs: This process is generally completed in about two weeks.

- Initiation of First Shipment, Import/Export