Overview

The basis for determining the customs value for Japanese imports is the Customs Tariff Law (in accordance with the WTO Customs Valuation Agreement).

As a general rule, import consumption tax and customs duties are imposed when an import declaration is made, and they are calculated by multiplying the import declaration price by the applicable tariff rate. The determination of the import declaration price should be made by the importer under the importer's responsibility.

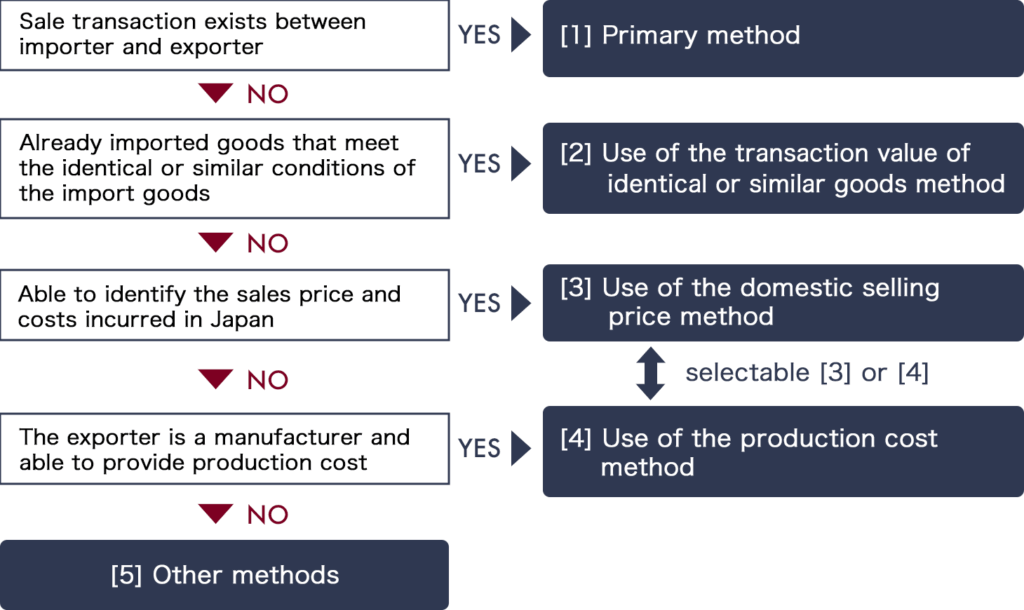

The import declaration price (customs value) is determined by the following steps.

※Please note that this article is drafted mainly to provide a high-level overview, and therefore does not describe details regarding Japan Customs Tariff Law.

Contact

Contact us 24 hours through the form

Recommended Content

[1] Primary method

(1) Outline

In principle, if the import is made based on the import transaction※1, we can use the primary method.

※1:Import transaction is a transaction in that a buyer in Japan makes a sale transaction with an overseas seller for shipping the goods to Japan, and the goods actually arrive in Japan.

Please bear in mind that the Invoice Value is not always equal to the Customs Value.

This Primary method is to calculate the Customs Value based on the "Value of the Import Transaction".

The definition of "Value of the Import Transaction" is that, when the import transaction of the imported goods has been made, the price actually paid or payable regarding the import transaction by the buyer to or for the benefit of the seller for the import goods, and adjusted by certain additional costs such as transportation costs, to the extent that such costs have not been included in the price actually paid or payable for the imported goods.

Calculation formula

Customs value = Transaction value = Actually paid or payable※2 + Additional costs※3

※2: The price actually paid or payable is the total payment made or to be made by the buyer to or for the benefit of the seller for the imported goods. It includes a settlement by the buyer whether in whole or in part, of a debt owed by the seller and other indirect

payment for the seller by the buyer. In principle, the price actually paid or payable shall not include the following charges or costs, provided that they are distinguished from the price actually paid or payable for the imported goods:

1) Charges for construction, erection, assembly, maintenance or technical assistance is undertaken after importation of the imported goods;

2) Transportation costs after importation;

3) Duties and taxes imposed on the imported goods in Japan.

However, if the price actually paid or payable will not be able to be grasped by the whole amount including the above costs, then it shall be the total amount including such costs.

※3:For instance, transportation fee and insurance fee (CIF basis), commissions, etc.

(2) Documents to be prepared

In the case of calculating the Customs value based on the transaction value, the calculation of the customs value should be based on invoices and other documents which are able to verify the price actually paid or payable of the imported goods and to be adjusted certain additional costs such as the transportation costs.

The principle determination method cannot be used for certain import cases, for instance, if there is no sales transaction, goods are traded free of charge, etc. In these cases, the following alternative methods are applied for the determination of the Customs Value.

[2] Use of the transaction value of identical or similar goods method

(1) Outline

If you already imported identical or similar goods, the customs value can be determined by using those goods if the following conditions are met.

Conditions of being identical goods

- The imported goods should have been exported approximately within one month before or after the export date of the target import goods.

- The imported goods should have been produced in the same country as the target import goods.

- The imported goods should have an identical shape, quality and value as the target import goods.

Conditions of being similar goods

- Same requirement as previously mentioned 1.2. in identical goods.

- The imported goods have similarities in terms of shape, component and functions. And it should be interchangeable with the targeting import goods.

(2) Documents to be prepared

- The materials to prove the identity and similarity. e.g. specification document, photos.

- The customs clearance documents related to the referenced identical / similar goods, such as invoice, import permissions.

[3] Use of the domestic selling price method

(1) Outline

In case of customs value cannot be determined by the previous methods, the determination method [3] using the domestic selling price or [4] using of the production cost can be applied. Upon request by importer, the priority of between [3] and [4] are selectable.

If we look at the [3] use of the domestic selling price method, the calculation is made as follows.

Customs value = Domestic selling price※4 - (general expenses required for the domestic sales of identical / similar goods, domestic transportation costs, and paid taxes & customs duties etc.)

(2) Documents to be prepared

- The evidence to prove the domestic selling price

- The materials to prove the domestic expenses (Invoice receipt from logistic companies, invoice receipt to confirm the paid taxes & customs duties)

Contact

Contact us 24 hours through the form

Recommended Content

[4] Use of the production cost method

(1) Outline

When the manufacturing cost of the imported goods can be identified, the customs value can be determined as follows.

Customs value = Production cost of the import goods + (general profits and expenses of export sales of identical / similar goods and the transportation costs until arrival at the port in Japan)

(2) Documents to be prepared

- The evidence to prove the manufacturing cost, such as the accounting ledger of the producer

- The materials to prove the profit and expenses added to the production costs, such as invoices

[5] Other methods

(1) Outline

If the methods mentioned previously cannot be used, Other methods will be applied.

In practice, these other methods are applied in many cases.

The Circular on the Customs Tariff Law, lists the following methods as example.

- Flexible application of the method prescribed in Article 4 of the Customs Tariff Law

- Calculating customs value by flexibly applying the method prescribed in Article 4-2 (identical/similar) of the Customs Tariff Law

- Calculating the customs value by flexibly applying the method prescribed in Article 4-3(1) (Domestic Sales Price) of the Customs Tariff Law

- Other flexible determination methods

Please feel free to contact us if you would like to discuss anything regarding your customs valuation issues.

Contact

Contact us 24 hours through the form

Recommended Content

Track Record – Attorney for Customs Procedures (ACP) Services

We have supported import and export operations in Japan for over 200 clients across more than 40 countries.

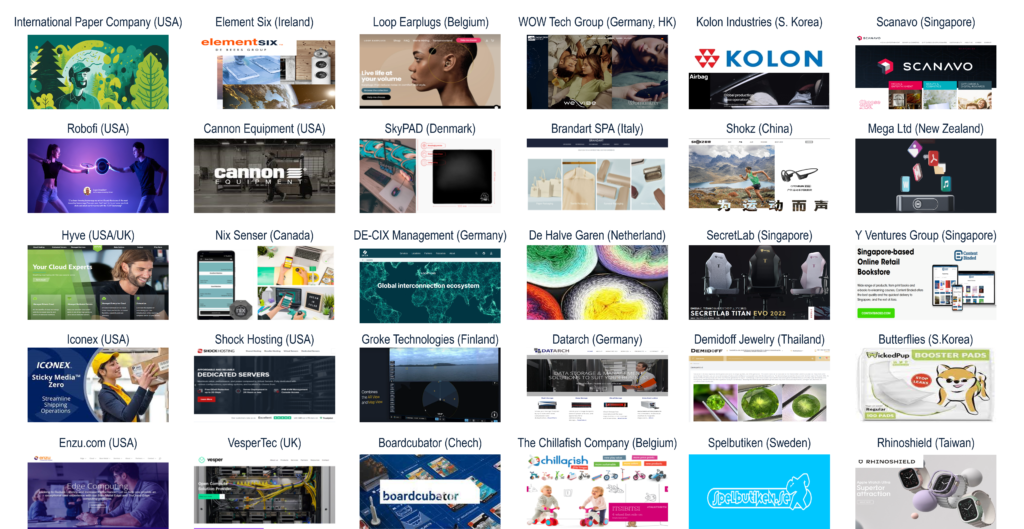

Examples of International Logistics Partners We Have Worked With

We have a proven track record of working with a wide range of logistics providers. As the Attorney for Customs Procedures (ACP), we handle customs-related responsibilities while logistics companies manage transportation and warehousing operations.

- American Overseas Transport (AOT)

- Apex International

- Brink's

- CEVA Logistics

- Coshipper

- Crane Worldwide Logistics

- DB Schenker

- DGX (Dependable Global Express)

- DHL Express

- DHL Global Forwarding

- Dimerco

- DSV Air & Sea

- Expeditors

- FedEx Express

- FERCAM

- GOTO KAISOTEN Ltd.

- Harumigumi

- Herport

- ICL Logistics

- JAS Forwarding

- Kintetsu Express

- Kokusai Express

- Kuehne + Nagel

- Mitsubishi Logistics

- MOL Logistics

- Nankai Express

- Nippon Express

- OIA Global

- PGS

- Rhenus Group

- Röhlig

- Sankyu

- Sanyo Logistics

- Scan Global Logistics

- Seino Schenker

- SEKO Logistics

- Shibusawa Logistics Corporation

- Shin-Ei gumi

- Shiproad

- Sumitomo Warehouse

- UPS

- UPS Supply Chain Solutions

- Yamato Transport

...and many other logistics providers in Japan and around the world.

Contact

Contact us 24 hours through the form

Recommended Content