Question 1: What kind of method shall be applied to the calculation of the Customs Value of the import goods?

The "Transaction Value Based Method (Actually paid or payable + Additional costs)" under the Japan Customs Tariff Law is the primary method that should be initially considered for application.

Please bear in mind that the Invoice Value is not always equal to the Customs Value.

This primary method is to calculate the Customs Value based on the "Value of the Import Transaction".

The definition of "Value of the Import Transaction" is the price actually paid or payable by the buyer to or for the benefit of the seller for the imported goods when the import transaction has been made, adjusted by certain additional costs such as transportation costs, to the extent that such costs have not been included in the price actually paid or payable.

Customs value = Transaction value = Actually paid or payable※1 + Additional costs※2

※1: The price actually paid or payable is the total payment made or to be made by the buyer to or for the benefit of the seller for the imported goods. It includes a settlement by the buyer whether in whole or in part, of a debt owed by the seller and other indirect payment for the seller by the buyer. In principle, the price actually paid or payable shall not include the following charges or costs, provided that they are distinguished from the price actually paid or payable for the imported goods:

1) Charges for construction, erection, assembly, maintenance or technical assistance is undertaken after importation of the imported goods;

2) Transportation costs after importation;

3) Duties and taxes imposed on the imported goods in Japan.

However, if the price actually paid or payable will not be able to be grasped by the whole amount including the above costs, then it shall be the total amount including such costs.※2:For instance, transportation fee and insurance fee (CIF basis), commissions, etc.

In calculating the Customs Value based on the transaction value, the calculation should be based on invoices and other documents that verify the price actually paid or payable for the imported goods and allow for the adjustment of certain additional costs such as transportation costs. In cases where the price actually paid or payable cannot be fully determined without including the above costs, the customs value shall be determined as the total amount including such costs.

You can find an explanation of what constitutes an “Import Transaction” in Question 2.

Q&A for Customs Valuation

Recommended Content

Contact

Contact us 24 hours through the form

Why choose us?

We specialize in navigating complex issues at the intersection of customs procedures and taxation—an area where our ability to offer practical, comprehensive support from both perspectives sets us apart. Understanding the close relationship between customs duties and national taxes (especially, Japan Consumption Tax - JCT), and addressing both in an integrated manner, is crucial in the context of international trade.

- Customs and International Trade Professionals - Led by our CEO, Mr. Sawada—Certified Customs Specialist and former KPMG professional—SK Advisory provides expert-level support in Customs and international trade. Mr. Sawada also serves as an external expert for the World Bank’s B-READY project in the field of customs and international trade.

- Full Compliance with Japanese Customs Law - We ensure full adherence to Japanese Customs Law, including Importer of Record (IOR) structure, HS code classification, and customs valuation. We assist in preparing all essential shipping documents for non-resident entities.

- One-Stop Support for ACP and JCT Tax Representative Services - In collaboration with trusted partner tax accountants, we provide comprehensive support for both customs procedures through the Attorney for Customs Procedures (ACP) and Japan Consumption Tax (JCT) filings through the JCT Tax Representative.

- Multilingual Communication - Our team communicates fluently in English, Japanese, and Chinese, offering smooth coordination with global clients and authorities in Japan.

- Support for Regulated Products - Our ACP/IOR partnership system can manage regulated items, including cosmetics, PSE-products, foodstuffs, and tableware.

- Trusted by Global Clients - Serving around 100 ACP clients annually, including many Amazon sellers, we’re a certified provider on Amazon SPN (Service Provider Network) under Trade Compliance.

Track Record – Attorney for Customs Procedures (ACP) Services

We have supported import and export operations in Japan for over 200 clients across more than 40 countries.

Examples of International Logistics Partners We Have Worked With

We have a proven track record of working with a wide range of logistics providers. As the Attorney for Customs Procedures (ACP), we handle customs-related responsibilities while logistics companies manage transportation and warehousing operations.

- American Overseas Transport (AOT)

- Apex International

- Brink's

- CEVA Logistics

- Coshipper

- Crane Worldwide Logistics

- DB Schenker

- DGX (Dependable Global Express)

- DHL Express

- DHL Global Forwarding

- Dimerco

- DSV Air & Sea

- Expeditors

- FedEx Express

- FERCAM

- GOTO KAISOTEN Ltd.

- Harumigumi

- Herport

- ICL Logistics

- JAS Forwarding

- Kintetsu Express

- Kokusai Express

- Kuehne + Nagel

- Mitsubishi Logistics

- MOL Logistics

- Nankai Express

- Nippon Express

- OIA Global

- PGS

- Rhenus Group

- Röhlig

- Sankyu

- Sanyo Logistics

- Scan Global Logistics

- Seino Schenker

- SEKO Logistics

- Shibusawa Logistics Corporation

- Shin-Ei gumi

- Shiproad

- Sumitomo Warehouse

- UPS

- UPS Supply Chain Solutions

- Yamato Transport

...and many other logistics providers in Japan and around the world.

Contact

Contact us 24 hours through the form

Recommended Content

Japanese Customs System Reform: Clarification of Importer Definitions

Starting October 1, 2023, Japanese Customs has instituted a pivotal reform aimed at addressing the issue of foreign sellers improperly designating third parties (such as forwarders or customs agents) as importers.

This revision necessitates foreign corporations to utilize an Attorney for Customs Procedures (ACP) to assume the role of Importer of Record (IOR) directly in many cases. The practice of merely nominally appointing another entity as the importer is no longer feasible.

Notably, foreign corporations that act as importers themselves, through the engagement of ACP, are eligible for Japan Consumption Tax (JCT) benefits. (link: Consumption Tax Treatment and Benefits of Using ACP).

As a dedicated ACP firm, we ensure compliance with the law to facilitate correct import procedures, allowing you to trust us with your importation requirements confidently. We are eager to engage in further discussions with you.

Revisions Effective October 1, 2023:

Definition of the Importer

- Regarding a cargo imported under import transaction, an importer is equivalent to “a person who imports a cargo” defined in Article 6-1 (1), General Notification of the Customs Act. ….. This means, the Consignee, etc., in the case of imports conducted through normal transactions between an overseas seller and a Japanese buyer

- In the cases other than above, an importer is a Person Having the Right of Disposal of the import cargo at the time of import declaration. If there is another person who acts on the purpose of the import*, that person is also included:

In case of a cargo imported:

- under lease contracts, a person who rents and uses the cargo.

- for consignment sales, a person who sells the cargo in the name of himself/herself (consignee) by accepting the commission.

- for processing or repairing, a person who processes or repairs the cargo.

- for disposal, a person who disposes the cargo.

Importer Defined as the “Person Having the Right of Disposal”

One of the most notable aspects of the amendment is the clarification that the “person having the right of disposal” is regarded as the importer under Japan Customs law. The term “right of disposal” is similar to ownership, but not identical. Although there is no explicit definition in the customs-related legislation, according to Japan Customs, it refers to the authority to decide how the goods will be handled after being released into Japan—for example, whether to sell the goods or to enter into a sales contract.

For additional information, please refer to the following resources:

- Japan Customs: Leaflet(English) Revision of Import Declaration Items and Attorney for Customs Procedure (ACP) System

- English: Announcement from Japan Customs | Mandatory to Use ACP in Many Cases – Attorney for Customs Procedure

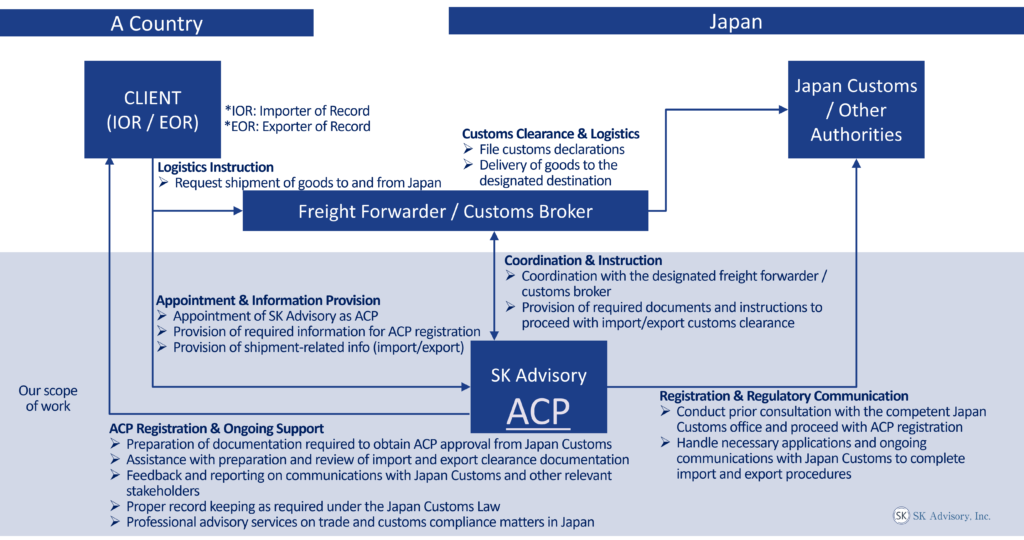

Our ACP Service: The Best Solution for the Japan Importer of Record (IOR)

ACP is an effective solution for addressing Importer of Record (IOR) and Exporter of Record (EOR) requirements in Japan. Through our ACP service, non-resident entities located outside Japan are able to import and export goods as Non-Resident IOR and EOR.

Below is an overview of our basic scope of work, together with a diagram illustrating the operational structure of the ACP service. Once ACP registration is completed, the non-resident entity can act as the Importer of Record (IOR) and Exporter of Record (EOR) in Japan.

Scope of Work – How We Can Assist

- Preparation and filing of all required documents for ACP registration with Japan Customs.

- Coordination and communication with relevant stakeholders, including Japan Customs, logistics providers, and customs brokers to ensure the smooth and compliant import and export procedures.

- Preparation and review of import documentation, including commercial invoices and shipping documents.

*Proper customs clearance requires accurate identification of the shipper, consignee / Exporter of Record (EOR), and Importer of Record (IOR) on B/L, AWB, and invoices. We provide practical guidance on correct documentation practices. We also advise on customs valuation (import declaration value) and its supporting documentation, HS classification, and country of origin to ensure compliance with Japanese customs requirements. - Advisory on customs valuation (import declaration value), HS codes, duty rates, and origin (including advance rulings).

- Import compliance support for regulated products, including Domestic Administrator (sometimes referred to as “Domestic Representative”) Services under the Product Safety Acts (PSE/PSC) and food-related products regulated under the Food Sanitation Act.

- Support for security export control, including list-based classification, catch-all control assessment, and assistance with export license applications to the Ministry of Economy, Trade and Industry (METI).

- Maintenance and retention of records required under the Japan Customs Law.

- Provision of professional trade and customs advisory services to address and resolve issues that may arise during import or export operations.

**Both import and export activities can benefit from the use of an ACP (Attorney for Customs Procedures). This support is applicable in scenarios where a non-resident acts as the Importer of Record (IOR) for imports and as the Exporter of Record (EOR) for exports.

Three Steps to Initiate Shipments Under the ACP Program:

- Quotation Review to Contract Conclusion: Upon receiving your contact details, we will promptly provide a quotation for your review.

- Commencing the Registration of ACP (Attorney for Customs Procedure) to Japan Customs: This process is generally completed in about two weeks.

- Initiation of First Shipment, Import/Export

Recommended Content

Contact

Contact us 24 hours through the form